The Divorce Financial Snapshot: What Goes Into the "Matrimonial Pot"?

Before you can split assets, you must value them. A practical checklist of what to gather for a UK divorce financial snapshot — from house equity to pension CETVs.

Written by

Divvio Editorial Team

Article author

Reviewed by

Divvio Content Review

Reviewed for consistency with Divvio's Form E product guidance and England & Wales financial remedy process content.

Last updated

Updated 12 May 2026

Reviewed and refreshed when the article or guide is materially updated.

Why Divvio is qualified to help

Divvio is built specifically for Form E and financial remedy workflows in England & Wales.

The product includes guided Form E steps, settlement and budget calculators, document checklists, and court-ready PDF generation.

This content is reviewed against the same explanations and workflows surfaced inside the app.

## In England and Wales, you can't sensibly negotiate a settlement until you've defined what exists and what it's worth.

Before you can discuss a 50/50 starting point (or any needs-based adjustment), you need a clear financial snapshot of the household's net position.

These are the same categories you'll disclose in Form E (or the relevant variant) — and missing something now can distort the conversation later.

Below is a practical checklist of the numbers to gather before you use a settlement calculator.

---

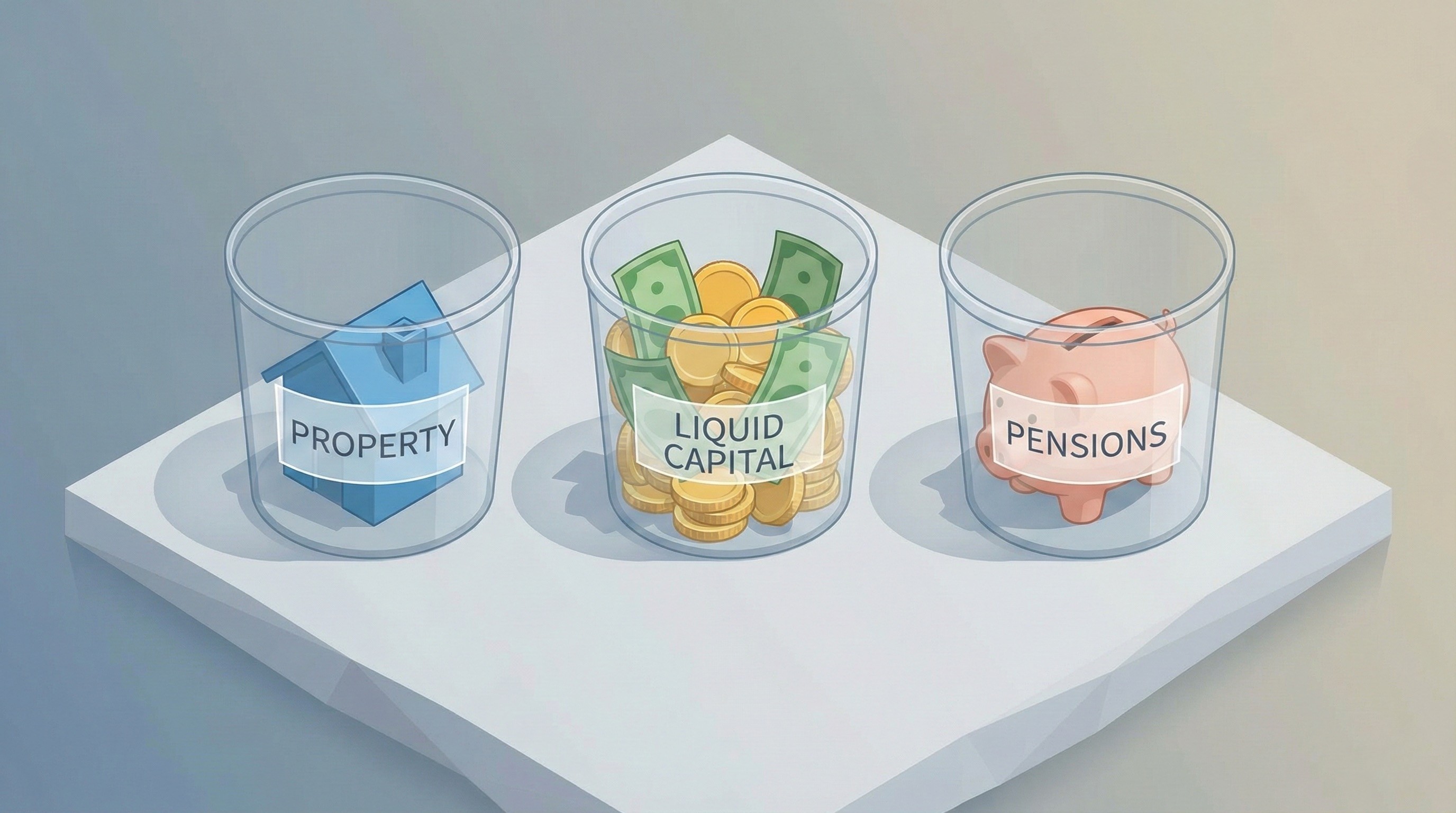

## The 3 buckets to capture your snapshot

For simplicity, it helps to group everything into three buckets. When using our [Divorce Settlement Calculator](/tools/divorce-settlement-calculator), enter these separately because they're handled differently in negotiation (especially pensions).

### 1) The housing bucket (property)

Usually the family home, but also buy-to-let property, holiday homes, and any land.

**The number you need:** Net equity (not just market value)

**A simple formula:** Market value – outstanding mortgage – estimated sale costs = net equity

> **Sale costs note:** If you're estimating, include estate agent + conveyancing costs (often around ~1–3% plus legal fees, depending on circumstances).

**Tip:** If you're unsure of value, use a recent agent appraisal or online estimate for now — just mark it as an estimate and update it later.

### 2) The liquid capital bucket (cash & easily realisable assets)

These are assets you can access relatively quickly.

**Includes:** bank accounts (joint and sole), ISAs, Premium Bonds, listed shares, and crypto.

> **Important:** You still disclose accounts held in your sole name. The disclosure stage is about full transparency, not what feels "private".

### 3) The pension bucket (illiquid capital)

Often the biggest asset after the house, and the easiest to undervalue.

**The number you need:** the Cash Equivalent Transfer Value (CETV). CETVs are a standard measure used to value pensions for divorce purposes. [GOV.UK](https://www.gov.uk/workplace-pensions/transferring-your-pension)

> **Common trap:** Don't use "projected income" or random figures from an annual statement if you've been told to provide a CETV. If you don't have one, request it from the scheme/provider.

---

## Debts & liabilities: what deducts from the pot?

A settlement is based on net wealth, so legitimate liabilities matter.

**Include:**

- Credit cards

- Personal loans / overdrafts

- Documented family loans (where it's clearly a loan, not a gift)

**Be careful with:**

- Informal "soft" family support that may be disputed as a gift rather than a debt

- Future living costs — these belong in your income needs budget, not your asset sheet

---

## The golden rule: full and frank disclosure

Financial remedy negotiations run on the duty of full and frank disclosure. If it later emerges that assets weren't properly disclosed, agreements can be challenged and the court can make adverse findings (including costs consequences).

If you're unsure about something, it's generally safer to list it and explain it than to omit it.

---

## Ready to run the numbers?

Once you've gathered figures for equity, cash, pensions, and liabilities, you're ready to see what the snapshot looks like.

👉 [Launch the Divorce Settlement Calculator](/tools/divorce-settlement-calculator)

---

## Related Articles & Tools

- **Article:** [The "Soft Loan" Trap: Is That Family Loan Really a Debt?](/blog/can-i-list-money-to-my-parents-on-form-e-the-soft-loan-trap)

- **Tool:** [Divorce Budget Calculator](/tools/divorce-budget-calculator) — Calculate your future income needs.

---

## Related Guides

- [How to calculate house equity for Form E](/blog/divorce-house-valuation-guide)

- [Not sure what to enter for pensions? Read the CETV guide](/blog/pension-cetv-guide-divorce)

Free checklist

Get the Form E document checklist by email

Every document you need to gather before starting Form E — bank statements, pension CETVs, valuations, income evidence — in one email you can work through.

One email with the checklist. No spam.

Ready to turn this into progress?

Start your Form E, test the settlement numbers, or use the complete guide for the next step.