Divorce Settlement Calculator UK: How to Calculate Your Split (The 3-Step Formula)

Calculate your divorce settlement split instantly. We explain the official 3-step legal formula: valuing the 'Matrimonial Pot,' applying the 50/50 sharing principle, and adjusting for 'Needs'. Stop guessing and start modeling your financial future.

Written by

Benedict Ayade

Article author

Reviewed by

Divvio Content Review

Reviewed for consistency with Divvio's Form E product guidance and England & Wales financial remedy process content.

Last updated

Updated 20 December 2025

Reviewed and refreshed when the article or guide is materially updated.

Why Divvio is qualified to help

Divvio is built specifically for Form E and financial remedy workflows in England & Wales.

The product includes guided Form E steps, settlement and budget calculators, document checklists, and court-ready PDF generation.

This content is reviewed against the same explanations and workflows surfaced inside the app.

## How is a divorce settlement calculated in the UK?

UK divorce settlements start at a 50/50 split of all matrimonial assets (the "matrimonial pot"), but this is adjusted based on each party's **needs**—particularly housing and income requirements. Courts consider factors like childcare responsibilities, earning capacity, age, and health to determine if one party needs more than half to meet their reasonable needs.

---

## The "50/50" Myth: Why There's No Simple Answer

You've Googled "divorce settlement calculator UK" because you want a number. A percentage. Something definite.

*"If we have £400,000 in assets, do I get £200,000?"*

Here's the uncomfortable truth: **maybe.**

Most people believe divorce is automatically 50/50. It's not. It's *"50/50... unless."*

Unless you have the children. Unless you can't work. Unless you earn significantly less. Unless the house needs to be kept for the kids. Unless one of you brought substantial assets into the marriage. Unless, unless, unless.

Online divorce calculators promise you a quick answer—plug in a few numbers, get your "fair share." But they're often dangerously misleading because they can't account for the **most important factor in UK family law: needs.**

The Family Court in England and Wales doesn't use a formula. It uses a **three-step framework** based on case law (particularly *White v White* and *Miller v Miller*). That framework is:

1. **What's in the pot?** (Calculate the matrimonial assets)

2. **What's the starting point?** (Apply the sharing principle—usually 50/50)

3. **Does anyone need more than half?** (Adjust for needs, particularly housing and income)

Let's walk through each step—and show you how to build a defensible settlement position *before* you sit down with solicitors.

---

## Step 1: Calculate the "Matrimonial Pot" (What Are We Splitting?)

You can't split what you haven't listed. This is why **full and frank financial disclosure** is the foundation of every divorce settlement in the UK.

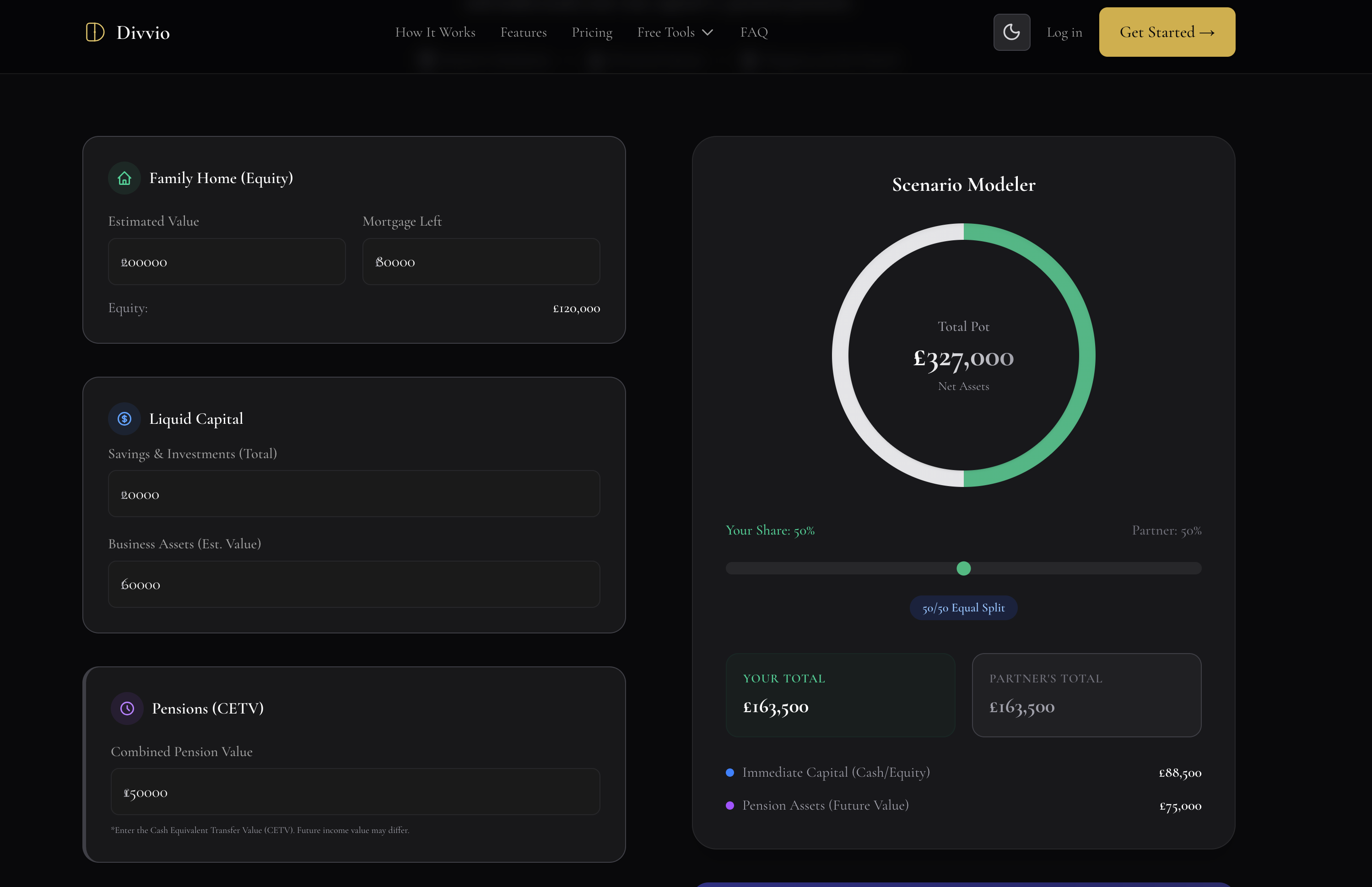

The "matrimonial pot" includes everything you and your spouse own—jointly or separately—acquired during the marriage. It corresponds directly to **Section 2 of Form E**, which is the court's official financial disclosure form.

Here's what goes into the pot:

### **Property Equity**

- **Family home:** Current market value minus outstanding mortgage

- **Buy-to-let properties:** Market value minus mortgage and estimated selling costs

- **Inherited property:** May be excluded if kept separate and not used for family benefit

### **Liquid Capital**

- **Bank accounts:** Current balance (all accounts, including ones "forgotten" by your ex)

- **Savings and ISAs:** Total value as of today

- **Investments:** Stocks, shares, bonds—use current market value, not what you paid

- **Cash:** Yes, even the £5,000 "emergency fund" hidden in the garage

### **Pensions**

This is the one most people forget—and it's often the **biggest asset** in the pot.

* You need the **Cash Equivalent Transfer Value (CETV)** for every pension—workplace, private, and SERPS/S2P

* State Pension (basic) is usually excluded, but Additional State Pension (SERPS/S2P) is included

* If you're over 40, your pension CETV might be worth more than your house equity

### **Business Interests**

* **Self-employed/Sole trader:** Net Asset Value (cash in bank + equipment – debts), NOT turnover

* **Limited company:** Value of shares, but most small companies have zero "goodwill" value

* **[See our guide on valuing your business correctly](https://www.divvio.co.uk/blog/self-employed-form-e-valuation-mistake)** to avoid the £100k mistake most freelancers make

### **Debts**

Subtract genuine liabilities:

* Mortgages (already deducted from property equity above)

* Credit cards, loans, car finance

* Tax owed to HMRC (very important for self-employed)

* **NOT soft loans from family** unless you have a written contract and evidence of repayments

**Action Step:**

Don't calculate this on a napkin or in your head. Use a structured approach.

**[Try our free Divorce Settlement Calculator](https://www.divvio.co.uk/tools/divorce-settlement-calculator)** to visualize your total matrimonial pot instantly. It walks you through every category and calculates your combined net worth in real-time—the same figures you'll need for Form E Section 2.

---

## Step 2: Apply the "Sharing Principle" (The 50/50 Starting Point)

Once you know the size of the pot, the law says: **start with equality.**

This principle comes from the landmark case *White v White* (2000), which established that there is no place for discrimination between the breadwinner and the homemaker. Both contributions—financial and domestic—are valued equally.

### **The Math**

If your matrimonial pot totals £500,000, the **starting position** is:

* **You:** £250,000

* **Your ex:** £250,000

If the pot is £150,000:

* **You:** £75,000

* **Your ex:** £75,000

Simple, right?

**Not quite.**

### **The Reality Check**

Here's where the sharing principle hits the real world:

Let's say you have £300,000 in total assets. A 50/50 split gives you both £150,000.

But ask yourself:

* Can you buy a 2-bedroom house in your area for £150,000 to live in with your two children?

* Can your ex rent somewhere suitable on their £18,000 salary with only £150,000 to their name?

If the answer is no, the court doesn't just shrug and say *"tough luck, equality matters most."*

**Needs trump sharing.**

If one party (usually the one with the children or lower income) **needs** more than 50% of the pot to meet their basic housing and living requirements, the court will adjust the split.

This is where divorces stop being 50/50 and start being 60/40, 65/35, or even 70/30.

---

## Step 3: Adjust for "Needs" (Why the Split Changes)

This is the **most important step**—and the one online calculators completely ignore.

**Needs** are defined as:

* **Housing needs:** Can you afford somewhere suitable to live (and house the children, if applicable)?

* **Income needs:** Can you meet your reasonable monthly living costs?

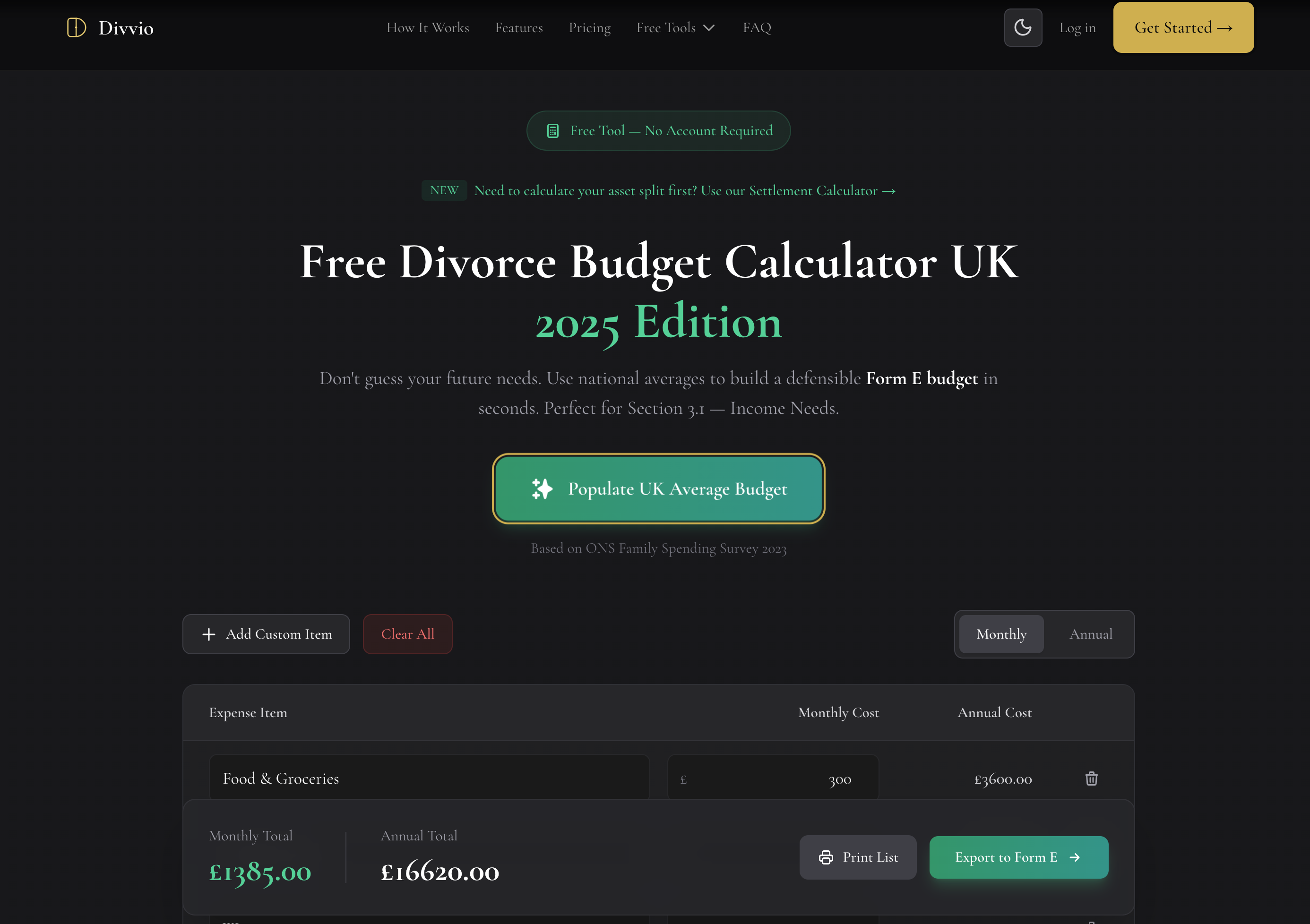

This corresponds to **Section 3 of Form E**, where you must set out your detailed monthly budget and future capital requirements.

### **How "Needs" Shift the Split**

Here's a real-world example:

**The Assets:**

* Family home equity: £300,000

* Your pension: £80,000

* Ex's pension: £40,000

* **Total pot:** £420,000

**The 50/50 Starting Point:**

* You each get £210,000

**The Needs Argument (Your Ex's Position):**

* "I have the children living with me full-time."

* "I earn £22,000/year; my ex earns £65,000/year."

* "I need a 3-bedroom house near the kids' school, which costs £280,000 in this area."

* "I cannot afford that on £210,000 and a mortgage."

**The Court's Likely Decision:**

* Your ex gets the **house** (£300,000) plus £20,000 cash = **£320,000** (76% of the pot)

* You keep your **pension** (£80,000) plus £20,000 cash from the ex's pension = **£100,000** (24% of the pot)

This isn't "unfair"—it's **needs-based**. Your ex cannot house the children on 50%. You can rebuild wealth through your higher income and pension. The court prioritises the children's stability.

### **Factors That Increase Your "Needs" Claim:**

* **Primary carer for children** (you need a bigger house)

* **Lower earning capacity** (part-time work, career break, age)

* **Health issues** (disability, long-term illness)

* **Age** (harder to rebuild wealth at 58 than 35)

* **Standard of living during marriage** (if you always had a cleaner, gym membership, private school fees, the court won't expect you to live in poverty)

### **How to Prove Your Needs**

You cannot just say *"I need more money."* You must **evidence** your needs with:

* A detailed monthly budget (rent/mortgage, utilities, food, childcare, car costs, insurance, etc.)

* Evidence of local housing costs (Rightmove listings for 3-bed homes in your area)

* Evidence of your income (payslips, tax returns, Universal Credit statements)

Guessing these figures is dangerous. If you underestimate your needs, you'll struggle to survive post-divorce. If you overestimate, the court will think you're being greedy or dishonest.

**Action Step:**

**[Use our ONS-backed Divorce Budget Calculator →](https://www.divvio.co.uk/tools/divorce-budget-calculator)** to build a defensible, evidence-based breakdown of your future income needs. It pre-fills UK national averages for groceries, utilities, council tax, and more—so you start with realistic figures, not guesses.

---

## FAQ: Divorce Settlement Questions

### **Does my ex automatically get half my pension?**

No. Pensions are part of the matrimonial pot and are considered for sharing, but they're often **offset** against other assets (e.g., you keep your pension, they keep more house equity). Pension sharing orders are common, but not automatic.

### **What if I owned the house before we married?**

Pre-marital assets can still be included in the pot—especially if they were used for family benefit (e.g., you sold your flat and bought the family home together). The longer the marriage, the less distinction courts make between "mine" and "ours."

### **Can I get more than 50% if I earn more?**

Unlikely, unless your ex's needs are very low. Earning more doesn't entitle you to a bigger share—it often means you're **expected to meet your own needs** while your ex gets more capital to compensate for lower income.

### **What if my ex hid money?**

If you suspect undisclosed assets, you can apply for a **Form E** to be filed under court order, request **bank statements and tax returns**, and even apply for **third-party disclosure** (e.g., from their employer or accountant). Lying on Form E is contempt of court and can result in the settlement being set aside.

### **Do I need a solicitor to work this out?**

Not always. Many couples negotiate settlements using **mediation** or **solicitor negotiation** without going to court. But you **must** complete full financial disclosure (Form E) to reach a legally binding agreement—even if you settle out of court.

---

## Conclusion: Stop Guessing, Start Filing

Here's the truth: no online calculator can give you a final answer. The court doesn't use a formula—it uses **discretion** based on your unique circumstances.

But you can take control of the process by:

1. **Using our Settlement Calculator** to understand the size of the matrimonial pot and see the 50/50 baseline

2. **Using our Budget Calculator** to evidence your genuine needs and see if you require more than 50%

3. **Filing Form E correctly** to make your position legally defensible

The problem? Most people try to do this in Word documents, spreadsheets, and scraps of paper—then spend £1,500+ on a solicitor to fix the mess.

**There's a better way.**

Divvio is the UK's first software tool that guides you through the **official Form E process** step-by-step—with built-in calculators, reality checks, and legal warnings that stop you from making costly mistakes.

* ✅ Automatic UK average budget pre-fill (ONS data)

* ✅ Business valuation warnings (stop the turnover trap)

* ✅ Soft loan detection (avoid the family debt mistake)

* ✅ Pension evidence checklists (get BR19 forms right first time)

* ✅ Court-ready PDF output (ready to file in 35 days)

**All for just £79.**

**[Start Your Form E with Divvio →](https://www.divvio.co.uk/eligibility)**

Stop guessing. Start filing. Get it right the first time.

---

*Divvio is not a law firm and does not provide legal advice. Every divorce is different, and settlements depend on individual circumstances. If you have complex assets, business interests, or international elements, consult a qualified family law solicitor. Divvio helps you complete the Form E document—it does not negotiate settlements or represent you in court.*

Free checklist

Get the Form E document checklist by email

Every document you need to gather before starting Form E — bank statements, pension CETVs, valuations, income evidence — in one email you can work through.

One email with the checklist. No spam.

Ready to turn this into progress?

Start your Form E, test the settlement numbers, or use the complete guide for the next step.